FINANCES, FUNDING

Enticing the Crowd: New Rules for Raising Capital Online

Joseph A. Davis, CDFA®

October 7, 2016

Equity crowdfunding platforms raised approximately $1.2 billion for U.S. start-ups in 2015, mainly from accredited investors — generally wealthy and sophisticated investors who meet certain criteria established by the Securities and Exchange Commission (SEC). That figure is expected to grow by 75% to 100% in 2016, with new SEC rules known as Regulation Crowdfunding that allow non-accredited investors to participate under specific conditions.1

How It Works

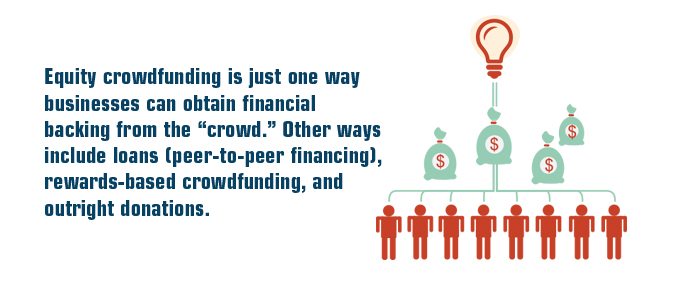

Crowdfunding is a nontraditional way to raise the money needed to launch or expand a small business. Instead of seeking a large cash infusion from an “angel investor” or venture capital firm, you could offer shares via an online funding platform to a larger group of people, each of whom takes a smaller stake in the company.

A funding portal could be used to explain your plans and attract investors, many of whom might be family members, friends, and customers in your own community. When equity is offered, your investors have a powerful incentive to promote your business among their own social networks.

Equity crowdfunding is just one way businesses can obtain financial backing from the “crowd”.

Small investors (incomes or net worth under $100,000) will be able to invest the greater of $2,000, or 5% of the lesser of their annual income or net worth. Individuals with both annual incomes and net worth of $100,000 or more can invest 10% of the lesser of their annual income or net worth, not to exceed $100,000 per year. Securities generally cannot be resold for at least one year and investors might have trouble selling shares if there isn’t a functioning secondary market.

New Rules in Play

A private company is generally allowed to raise a total of $1 million over a 12-month period through crowdfunding, presumably at a lower cost and with fewer regulatory requirements than a public offering.

Even so, crowdfunding companies must provide a long list of specific disclosures to the SEC, potential investors, and the intermediary that facilitates the transactions. Examples include the target offering amount, the fundraising deadline, descriptions of the business and its owners, the pricing of securities, and how the crowdfunding proceeds will be used. Financial statements may need to be accompanied by company tax returns and independently reviewed or audited.

Before making any investment commitment, an investor must attest that they have reviewed the intermediary’s educational materials and understand the investment is illiquid, there is no guarantee of any return, the entire amount of the investment may be lost, and are in a financial condition to bear the loss. Investors must also complete a questionnaire to demonstrate an understanding of the risks of any potential investment and other required statutory elements.

1) crowdexpert.com, 2016

The information in this article is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax or legal advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Emerald. Copyright 2016 Emerald Connect, LLC.

Follow These Two Rules to Build Wealth in Any Market

Throughout the past two and a half months I have continued to ask myself, did we jump off a financial cliff? The answer was no. How did I know? The answer, while somewhat complex, is profoundly simple.

Financial Planning in the Sandwich Generation

While it’s true that retirement accounts can be used to save for college, there may be negative consequences to doing so. It’s best to talk with a financial professional to determine the appropriate course of action and to make sure you’re on track to meet your goals.

Matchmaker: Maximizing Your Employer 401(k) Contributions

A 401(k) isn’t the only option for retirement, but it’s definitely one of the most attractive. In many cases, it offers free money and is relatively easy to roll over when you change jobs. A financial professional can help you prepare for retirement with a 401(k) that fits your current investment style and stage in life and adapts to changes in career or investment styles.

Splitting Retirement Nest Eggs During Divorce

Qualified plans, such as 401(k), profit sharing, defined benefit pension and money purchase pension plans, have defined benefits or defined contributions. A qualified domestic relations order, or QDRO, is required when dividing qualified plans.

Davis Financial LLC

A financial services firm servicing clients across Utah. We strive to understand your goals, help you manage your retirement planning, guide your overall wealth strategy and help minimize your tax liability through a long-term and trustworthy relationship.

Office Hours: M-F, 9am-5pm

Call Us: (801) 620-0586

Directions: Map It

Copyright © 2023 Davis Financial. All Rights Reserved.

This site is published for residents of the United States and is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any security or product that may be referenced herein. Persons mentioned on this website may only offer services and transact business and/or respond to inquiries in states or jurisdictions in which they have been properly registered or are exempt from registration. Not all products and services referenced on this site are available in every state, jurisdiction or from every person listed.

Securities offered through Purshe Kaplan Sterling Investments, Member FINRA & SIPC., Headquartered at 80 State Street, Albany, NY 12207. Advisory Services offered through BEAM Wealth Advisors, Inc., a SEC Registered Investment Advisory Firm. BEAM Wealth Advisors, Inc. is a separate entity from Purshe Kaplan Sterling Investments. Joseph Davis, Registered Representative, Aaron Schuler, Jr, Investment Advisor Representative, Beam Wealth Advisors, Inc., Tax services provided by Davis Schuler & Associates, LLC. Advisory services offered by Beam Wealth Advisors. Davis Financial LLC, Beam Wealth Advisors, Inc., Davis Schuler & Associates, LLC, and Purshe Kaplan Sterling Investments are separate, unaffiliated entities.